Health insurance 101: Making a health insurance claim in Thailand

The vast majority of people who purchase health insurance do so with the hopes that they remain healthy enough to not actually have to use the claim. The reality, however, is that with health insurance it is not a matter of if you will need to submit a claim, but when will you need to do so. Here, we take a look at the best ways you can submit a health insurance claim in Thailand, our latest infographic, and some important claim-related tips.

The basics of submitting a claim in Thailand (direct billing vs reimbursement)

Generally speaking, there are two ways you can submit a claim for almost all types of health insurance policies sold or used in Thailand:

- Direct billing

- Reimbursement

While both of these methods will see claims paid, there are marked differences between the two.

Submitting a claim using direct billing

Direct billing essentially means that the medical facility will bill the insurer before the patient. This claiming method is most often available on international plans and from larger insurers offering local plans in the country.

In order to facilitate this benefit on their insurance plans, health insurers have created a network of health facilities who have agreed to bill the insurer when a person with coverage receives care.

If you are going to go to a facility that offers direct billing with your plan, the general way to submit a claim is as follows:

- Make an appointment with the healthcare provider.

- Register at the clinic/hospital before receiving care.

- Present your ID, Hospital card (if you have one previously issued by the hospital), insurance card, and any other requested documents.

- Read and sign all paperwork.

- Receive care.

- Sign the bill.

- Go home.

Of course, there might be some additional steps or things to be aware of when using this method, we will cover the most important further down in this article.

Submitting a claim via reimbursement

This is the more traditional method of submitting a health insurance claim in Thailand. Generally speaking, it will involve more paperwork and, possibly legwork, but is still used by many insurers around the world. In many cases, this is the method of claim used when you receive care outside of your direct billing network.

The process for submitting a claim via reimbursement generally consists of the following steps:

- Make an appointment with the healthcare provider.

- Register at the clinic/hospital before receiving care.

- Present your ID, Hospital card (if you have one previously issued by the hospital), insurance card, and any other requested documents including a claim form.

- Read and sign all paperwork.

- Receive care.

- Pay your bill and collect the claim form from the doctor.

- Go home.

- Submit the form to the insurer either by mail, fax, online, or email.

- Wait.

Once you have submitted a claim for reimbursement the insurer’s claims team will start the reimbursement process and if it is accepted will issue payment either in cheque form or bank deposit (based on the method you select when you submit the claim).

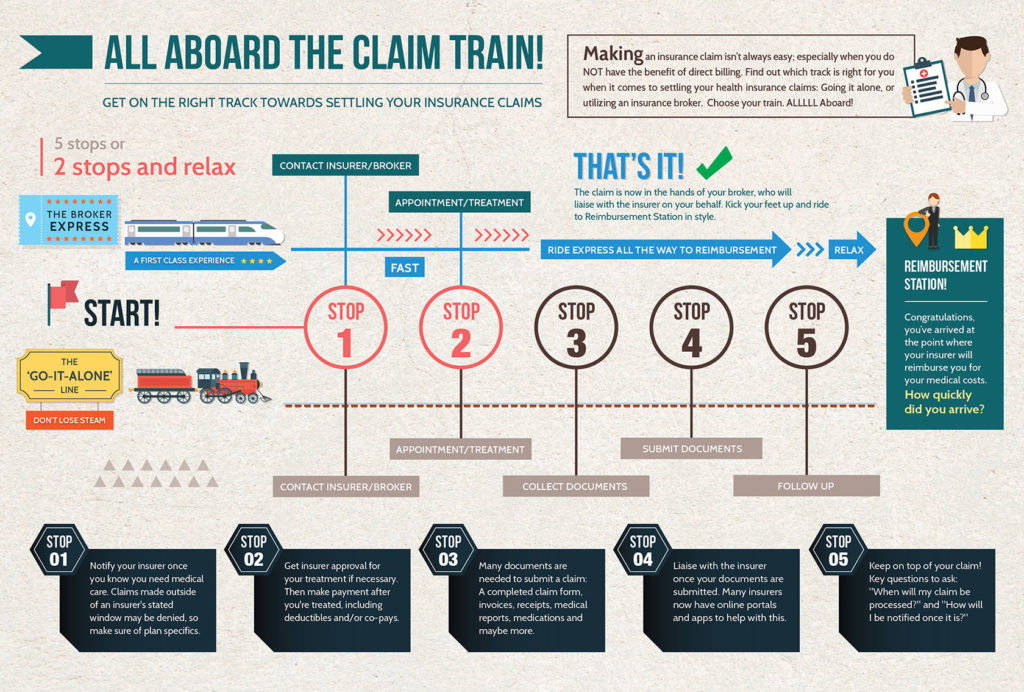

Looking at the clam train infographic

There is another method however, one which could help making a health insurance claim in Thailand easier: Use your broker. Many of the best brokers like Pacific Prime have set up a dedicated claims team who can help manage any and all claims. To help explain how, we have created the Claim Train infographic.

In this helpful little infographic, we explain not only the process of submitting a claim, but also how a broker like Pacific Prime can help when it comes to submitting a claim using international health insurance.

Check out the infographic on our main site today.

7 tips on how to ensure a health insurance claim in Thailand is successful

Here are seven tips that you can utilize to help ensure that any claims you submit are handled as efficiently as possible.

If you are using direct billing:

- Be sure to read your plan’s direct billing documentation – Most insurers will provide you with a list of medical providers that accept direct billing. It is therefore important to be aware of where they are in case you do need to see a doctor. Beyond that, this documentation will also usually include tips on any insurer specific terms that need to be met when using this benefit.

- For larger procedures talk to your insurer/broker first – While this is not essential for all insurers, it is usually preferred that before you receive care for expensive issues or ongoing treatments you first talk to the insurer and achieve pre-approval. This helps ensure the claim is processed quicker and also allows the insurer to potentially recommend a more cost effective location for care.

- Be aware of your plan’s limits and exclusions – It is important to point out here that direct billing does not mean your whole hospital bill is covered. Many insurers have limits on their plans and if you go over them, you will still be responsible for any overages. The same goes for excluded care. If you have a type of care or condition excluded by your plan, direct billing will not be accepted, or you will be required to pay the hospital after the insurer denies coverage – with some plans this might take months to sort out.

If you are going to submit a claim for reimbursement:

- Know what your plan covers – As with all types of care, it is important to know exactly what is and is not covered by your plan. Pay close attention to exclusions and level of cover along with exclusions or limits for certain providers or procedures.

- Know if there are any hospitals excluded – Many corporate health plans, and an increasing number of individual plans, are starting to implement cost saving measures. One of the most common is excluding care from listed High Cost Providers. Other insurers will only cover a certain percentage of the bill at these facilities. If you visit one of these providers, there is a high chance your insurer will reject the claim.

- Contact your insurer before you receive care – This will help save you time at the hospital. By contacting your insurer before you receive care they could work with the hospital to ensure the billing process goes smoothly and will even inform you about the cost and how much will be covered.

- Download your claim form before you see the doctor – To be clear here, this is not a necessity. Generally speaking, if you are going to submit a claim for reimbursement you can fill the claim form out after and attach any necessary paperwork e.g., diagnosis slips. That said, if you can get the doctor to fill out the form and sign it there is a good chance your claim will be processed with minimal back and forth. In short, this could make the process shorter.

Finally, the last tip here would be to talk with a broker like Pacific Prime. With a dedicated in-house claims team, we can help you manage the process and file a claim on your behalf. If you talk with us ahead of time, our team of experts can help not only recommend a suitable hospital but also important documents you will need to get. That is where the infographic listed above can really help.

To learn more about Pacific Prime and the claims process, visit the infographic page on our main site, or contact us today.

- Why children should have health insurance cover in Thailand - March 18, 2021

- Vaccinations for Thailand: An up-to-date list of all essential inoculations - January 27, 2021

- Important questions to ask about teacher’s health insurance in Thailand - January 26, 2021

Comments

Comments are disabled for this post